Since early 2018, Indian stock markets have behaved uniquely – whereas selective stocks have helped keep nifty near all-time highs, most of the stocks at broader level, have seen significant corrections.

The main reason behind this has been the ‘continued cautious sentiment’ over the last couple of years – due to varied factors – demonetisation, GST, political uncertainty, erratic monsoons, lower GDP, corporate shake-ups etc.

Result has been that of complete confusion and chaos.

People who are doubting the stock market itselfMost investors are either not sure to continue investing into stock markets or confused about which sectors to invest into

The stock market returns during this period are especially important as it has been a difficult and volatile period. We saw bull run followed by 2008 meltdown, UPA-1, UPA-2, Modi – 1, now Modi – 2, scams, NPAs, shake-ups, Brexit, Trump, Protectionism.

As an example, all of us know that Gold, Real Estate have done nothing in the last 5-6 years.

Besides, Real estate can be highly illiquid at times, is required to be maintained, carries completion risk and has significant tax leakages both at the time of buying (registration, brokerage) and selling (brokerage, capital gains).

If not confident yourself, there is always mutual fund route to let your money be managed by professional fund managers.

The big question – which sectors to invest into?Nowadays one gets to hear a lot of opinions around this – given the backdrop of declining GDP, weak auto sales, muted consumer sentiment, govt’s focus on infrastructure and global headwinds around IT and pharma sectors. Most of these opinions are primarily based upon spokesperson’s personal view about the overall stock market and his own likes and dislikes.

- Someone who is negative on the market, recommends to move towards defensives and invest in the Infromation Technology (IT).

- Someone who hates high Price-to-Earning (P/E) multiple sectors advises to avoid Fast Moving Consumer Goods (FMCG) and look somewhere else.

- Likewise, pure value investor recommends to go for infra, capital goods and pharma.

The idea here is to remove the personal biases and instead present some hard facts and try draw learnings from the same.

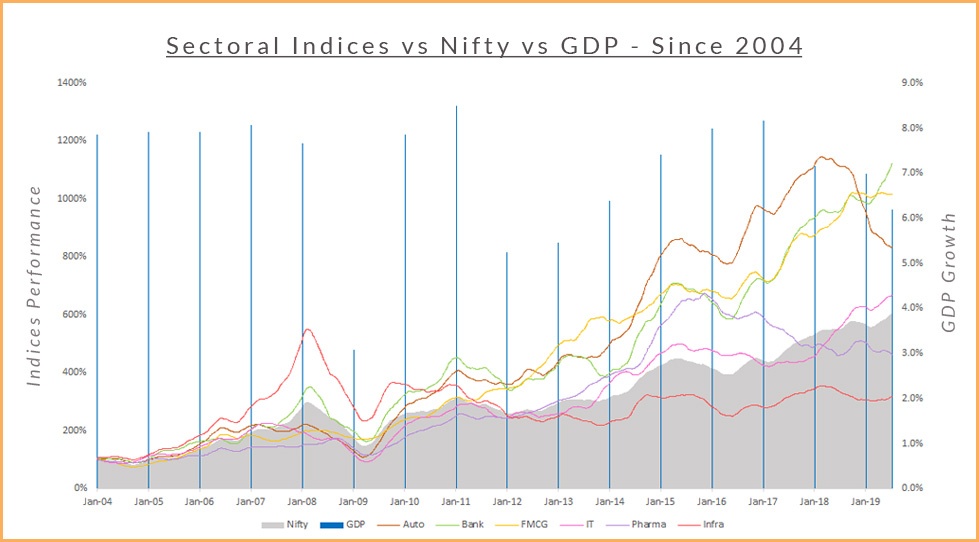

A. Historical Sector-Wise Performance vs Nifty vs GDP Growth

Key points to note from the above –

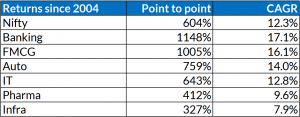

- Best performing and least volatile – Banking and FMCG – both have significantly outperformed the nifty. Out of the two, FMCG is less volatile compared to banking.

- Good but volatile – Auto – was best performing till Jan 2018 but has corrected significantly since then. The sector generally faces headwinds during weak GDP growth but recovers quickly as GDP revives. The sector is more volatile and witnesses higher number of twists and turns.

- As good as nifty – IT – considered as defensive is closest to the nifty performance. Surprising !

- Most volatile – Pharma – after underperforming nifty from 2004-12, had a significant outperformance from 2012-16, followed by a significant correction since 2016. The sector behaved as most volatile compared with the others. A big surprise again, as this sector along with IT is generally considered to be the safest.

- The worst performer – Infra – that also includes capital goods. Again this might be surprising to most given that infra is logically supposed to do well in a developing economy like ours. We will try to address this dichotomy in the next section.

B. Key Sector Characteristics Worth Considering before Deciding Banking

This sector provides leverage (debt) to businesses for growth and consumers for consumption. It is an intergal part of any economy.

Banking, therefore cannot underperform for long if the GDP has to continue to grow over sustained periods.

Key risks in banks – banks operate on high leverage (6-8 times) and their main fuel for growth is public money (i.e., deposits). Public money provides stability during normal course, but the same becomes any bank’s biggest headache during global or local panic situations. Likewise, during GDP slowdowns, as businesses start to retract, their dues towards banking system (interest and principal repayments on loans) gets delayed or worse defaults – affecting bank’s profitability, NPAs and balance sheet.

These situations can accordingly lead to stock price corrections in the impacted banks and can be brutal at times (e.g., Yes Bank recently, Axis and ICICI in the past). However, one can also keep in mind that the banks are of systemic importance to any country and hence you will rarely see banks getting closed (mergers are more likely).

My personal favorite and especially so in the Indian context. E.g., Dabur, Godrej, Nestle, Hindustan Lever, Britannia etc.

The sector caters to many non-discretionary (essential) requirements of a consumer and hence becomes the direct beneficiary of the Indian population exceeding 130 crore people.

The sector is also the easiest to understand, mostly well governed and has low debt levels.

Key risks in FMCG – the sector always trades at high P/E multiple and hence is doubted by many pundits. You will always see them trying to pull down the sector at the slightest of the opportunity and hence for short periods there can be negative downticks in some companies. The fact remains that over sustained period of time, all of them have been proven wrong.

I cannot imagine how India will achieve it’s truest economical potential ($5 trillion target) without consumers spending on the FMCG products.

The sector comprises of Passenger Vehicles (Cars, Two wheelers), Commerical Vehicles (Trucks, Buses) and Farm Vehicles (Tractors). E.g., Maruti, Bajaj Auto, Mahindra & Mahindra, TVS etc

The sector shares many characterisitics of the FMCG sector. However, there is one important difference and which is also the main risk as highlighted below.

Key risks in Auto – Spending on auto is discretionary in nature. As a result, various factors can create turbulences in the short to medium term. e.g., overall sentiment, monsoons, infra spending, industrial activity etc.

Besides, in the current scenario one also needs to keep in the mind the government’s push towards Electric Vehicles (EV) and increased competition from some well established global competition.

However, over long period of time, the Auto sector cannot move inversely to the economic growth.

It’s important to differentiate IT in India vis-a-vis say IT in US. Here it’s more service driven (e.g., Infosys, TCS), whereas in US it’s more product and innovation driven (E.g., Google, Facebook, Linkedin).

Service businesses generally help one create a sustained long term growth whereas product businesses command most premium in the market.

IT in India mostly is well governed and operates on low debt levels. Besides, we being having significant employable population with low income levels, will always have cost arbitrage and find services to be provided to the other countries.

Key risks in IT – Being majorly dependent on the international business, one needs to have knowledge of various variables – international politics, foreign exchange implications, long term vs short term contracts etc.

The most difficult sector for me to understand personally. I can’t even pronounce the names of it’s products !

Example of the companies – Sun Pharma, Cipla, Biocon etc.

This sector is again heavily export oriented because of the cost arbitrage and hence better margins.

On corporate governance and debt levels, the sector is a mixed bag.

There is also lot of product research and innovation happening in this sector but for a layman, it’s extremely difficult to draw actionable conclusions from that.

Key risks in pharma – The sector being directly linked with the well-being of humans, has tight regulatory controls globally. Consequently, there can be unexpected announcements, price controls, enquiries etc impacting stock prices over varying periods of time.

The sector comprises of roads, bridges, power, ports, telecom, logistics, capital goods etc.

Example of the companies – Tata Power, Dilip Buildcon, BHEL, Concor etc.

Good Infrastructure development is both cause and effect of the economic growth and therefore play a very imporant role in a developing country like India. The sector got it’s deserved attention till 2008, but has been underpforming since then due to the factors as highlighted below.

Key risks in infra – All Indian governments have consistently focused on infrastructure development in the country (though one can argue about actual vs potential). However, this sector continues to be impacted by too many factors – policies, approvals, land acquisition, tariffs, receivables, high debt, corporate governance etc etc etc.

I hope that the above is helpful for you to choose the right sector for yourself.

Every sector will have every kind of companies – investible as well as non-investible. Sector is important to understand the overall contours in which a company operates – and therefore to make a proper risk adjusted investment suiting an individual’s own investing style.

Different investors work with different time frames, different risk appetite and different skill sets.

Disclaimer: These are my personal views and not any recommendation to the reader. The reader should do his own independent research before taking any investment related decision.